Category: Financing

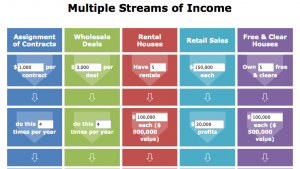

Multiple Streams of Income Calculator

I love income. And I’m not afraid to say it. How does it get better? MULTIPLE streams!

Rules and Regulations of Self-Directed IRAs

IRAs can be tax free or tax deferred. Do you use them? They’re a FABULOUS way to invest in real estate.

Mortgage Closing Costs are on the Rise

Have you noticed a change in fees? Do you know how to buy real estate without going to a traditional lender?

Using a Credit Card to Finance Deals

Have you ever used a cash advance on your credit cards to finance a real estate deal? Consider this:

Stop Saving for Your Future

Stop saving for your future, which seems far away. Here’s why you focus on today:

Finding Private Money – It’s Easier Than You Think

We have never solicited private funds but we have private money lenders from around the country. How?

Why Being Broke Can Be Good for Your Investing Business

The best investors operate “as if” they’re broke even when they no longer are. But why?

Financing Investment Property

How do you go about finding financing for an investment property? A few options include:

Pre-qualification vs. Pre-approval

Pre-qualification vs. Pre-approval – do you know the difference and does it matter?

Questions to Expect when Applying for a Mortgage

Applying for a mortgage? If so, it’s important that you get specific information in order before approaching a lender.

Foreclosures – More Profitable Than Loan Modifications?

These perks give servicers little incentive to offer loan mods, and some incentive to push loans into foreclosure.

Find out more about my books: