Category: Credit

What Credit Score do You Need to Get a Loan?

When applying for credit, one of the first things you need to know is your credit score.

But why?

Your Credit Score May Sink When You Sign up for Mortgage Relief

What are these mortgage assistance programs?

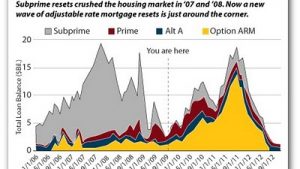

Mortgage Resets – Here comes the next wave

I know everyone really wants to believe the housing market is going to get better in 2010. I know we’ve all had enough of the gloom and doom, but it appears we have to brace ourselves for more of the same, at best. We’re so […]

How do you Protect What you Have?

With the implosion of the housing market, the collapse of credit, how do you protect what you have?

Turned Down for a Mortgage? What’s Next?

About half of all mortgage applicants are being turned down. The rules keep changing. Don’t give up.

Debit Card – Do You Use One?

But we haven’t talked about Debit Cards. Do you use one? Do you know the danger if you do?

Your Credit Card is Canceled

However, canceling cards without warning is allowed. What can you do about it?

Raising Your Credit Score after a Short Sale

How does a short sale affect your credit report and is there anything you can do about it?

How to Increase Your Credit Score

Read on to learn how to increase your credit score and why it’s important that you do.

Find out more about my books: