Category: Financing

What Credit Score do You Need to Get a Loan?

When applying for credit, one of the first things you need to know is your credit score.

But why?

Mortgage Rates – Do You Care?

We’ve gotten so used to having low rates that they no longer encourage buyers. But who cares??

How to Accelerate Your Mortgage Payoff – follow-up

I recently wrote: How to Accelerate Your Mortgage Payoff. I hope you will try this technique and see the amazing results for yourself.

How to Accelerate Your Mortgage Payoff

Here are some methods to make extra payments work to your advantage and get the most credit for any additional monies you send in.

Interest Rate Discussion

When qualifying for a mortgage, of primary concern is your interest rate. Know what your lender charges for a loan.

Tax Statements and Private Money Lenders

When lending and borrowing, are you mailing and/or receiving 1098’s or 1099’s? Do you know how to use them?

Seller Financing Escapes Extinction

As worded now, a private seller, trust or estate can provide seller financing 3 times per 12 months.

How Many Ways can Lenders Prevent a Closing?

I do not want to know. However, I did just find one more answer to add to my list of personal experiences.

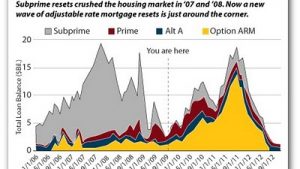

Mortgage Resets – Here comes the next wave

I know everyone really wants to believe the housing market is going to get better in 2010. I know we’ve all had enough of the gloom and doom, but it appears we have to brace ourselves for more of the same, at best. We’re so […]

Turned Down for a Mortgage? What’s Next?

About half of all mortgage applicants are being turned down. The rules keep changing. Don’t give up.

Reverse Mortgage – Good Thing or Bad?

A reverse mortgage provides income for people to tap into for their retirement. Is that good?

Find out more about my books: